ARTICLE | May 21, 2024

Authored by RSM US LLP

Do you have assets you expect to grow significantly? Leaving such assets in your estate to appreciate during your lifetime may increase your estate tax bill. However, if you have already utilized your current available lifetime gift tax exemption, making an outright transfer and triggering gift tax might not be the most desired option. A Grantor Retained Annuity Trust (GRAT) can be a valuable tool to address this. It allows you to transfer wealth to future generations while freezing the current value of the assets for tax purposes and using minimal lifetime gift tax exemption.

What is a GRAT?

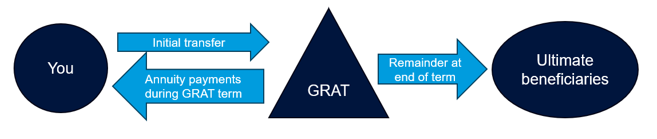

A GRAT is an irrevocable trust that exists only for a specified period of time. You initially transfer assets to the GRAT and then receive annuity payments back for the term of the GRAT. For example, you transfer an asset worth $1 million to the GRAT. Over the term, the GRAT pays you $999,999 of annuity payments. This results in a $1 ‘taxable gift.’ If the assets appreciate more than the annuity payment back to you, the excess appreciation escapes your estate transfer tax free. If the $1 million of GRAT assets grows to $1.5 million during the term, that $500,000 of growth will pass to your beneficiaries free of estate and gift tax. At the end of the specified term, the GRAT terminates, and the remaining assets are transferred to the GRAT beneficiaries (typically a younger generation), either outright or in trust.

What are the requirements for establishing a GRAT?

- The annuity payments must be:

- Either a fixed dollar amount or a set percentage of the initial value of the transferred assets.

- Paid to the grantor at least annually.

- Payable for a fixed term (e.g., 2, 5, 10 years).

- Made only to the grantor or grantor’s estate.

- The annuity payments cannot:

- Be prepaid by the GRAT.

- Be paid via loans.

- Increase more than 20% from the prior year’s payment.

- After the initial GRAT funding, no additional contributions can be made.

What are the benefits of setting up a GRAT?

- If the assets grow at a rate greater than the annuity rate specified by the IRS (the “hurdle rate” or “7520 rate”), that excess growth accrues to the beneficiaries transfer tax-free.

- During the term of the GRAT, you are treated as the owner of the assets for income tax purposes. Thus, you are responsible for paying income tax on the GRAT income. Paying income taxes on behalf of the GRAT is not considered an additional gift to the GRAT. The GRAT is able to grow without being reduced by the payment of income taxes, leaving more to pass to your beneficiaries.

- Generally, GRATs can even hold shares in S corporations.

What are the potential downsides to setting up a GRAT?

- If you die during the GRAT term, the assets go back to your estate, negating the transfer tax benefits.

- If your assets don’t grow as much as expected (or even lose value), little or no assets may remain for the beneficiaries at the end of the GRAT term.

- GRATs are generally not effective for transfers to grandchildren because the generation-skipping transfer (GST) tax rules may require you to use an excessive amount of GST exemption. Thus, GRAT assets are usually left to only children.

- When your beneficiaries inherit the assets, they inherit the original tax basis you had. This might not be ideal for assets with low basis, meaning the beneficiaries could owe more capital gains tax when they eventually sell.

Is a GRAT right for you?

GRATs can be a strategic way to transfer wealth to beneficiaries. However, the length of the GRAT term, the specific assets to be contributed to the GRAT, the beneficiaries of the GRAT and the IRS hurdle rate at the time the of the initial gift should all be carefully considered. The benefits and risks of a GRAT can vary greatly based on these factors and should always be adjusted for a grantor’s individual circumstances. By understanding the requirements, advantages, and potential downsides, you can make an informed decision about whether a GRAT is right for your estate planning needs. As always, consult with your RSM US tax advisor to tailor a strategy that best suits your situation and goals.

This article was written by Scott Filmore, Amber Waldman and originally appeared on 2024-05-22.

2022 RSM US LLP. All rights reserved.

https://rsmus.com/insights/tax-alerts/2024/grantor-retained-annuity-trusts-explained.html

The information contained herein is general in nature and based on authorities that are subject to change. RSM US LLP guarantees neither the accuracy nor completeness of any information and is not responsible for any errors or omissions, or for results obtained by others as a result of reliance upon such information. RSM US LLP assumes no obligation to inform the reader of any changes in tax laws or other factors that could affect information contained herein. This publication does not, and is not intended to, provide legal, tax or accounting advice, and readers should consult their tax advisors concerning the application of tax laws to their particular situations. This analysis is not tax advice and is not intended or written to be used, and cannot be used, for purposes of avoiding tax penalties that may be imposed on any taxpayer.

RSM US Alliance provides its members with access to resources of RSM US LLP. RSM US Alliance member firms are separate and independent businesses and legal entities that are responsible for their own acts and omissions, and each are separate and independent from RSM US LLP. RSM US LLP is the U.S. member firm of RSM International, a global network of independent audit, tax, and consulting firms. Members of RSM US Alliance have access to RSM International resources through RSM US LLP but are not member firms of RSM International. Visit rsmus.com/aboutus for more information regarding RSM US LLP and RSM International. The RSM(tm) brandmark is used under license by RSM US LLP. RSM US Alliance products and services are proprietary to RSM US LLP.

|

Thomas Howell Ferguson P.A. CPAs is a proud member of RSM US Alliance, a premier affiliation of independent accounting and consulting firms in the United States. RSM US Alliance provides our firm with access to resources of RSM US LLP, the leading provider of audit, tax and consulting services focused on the middle market. RSM US LLP is a licensed CPA firm and the U.S. member of RSM International, a global network of independent audit, tax and consulting firms with more than 43,000 people in over 120 countries. Our membership in RSM US Alliance has elevated our capabilities in the marketplace, helping to differentiate our firm from the competition while allowing us to maintain our independence and entrepreneurial culture. We have access to a valuable peer network of like-sized firms as well as a broad range of tools, expertise, and technical resources. For more information on how the Thomas Howell Ferguson P.A. CPAs can assist you, please contact us. |